Spring 2022 The Retirement Plan Company Newsletter is here and with it comes a new edition of The Retirement Plan Company Newsletter. This issue is packed with information to help you stay informed and up-to-date on your retirement plan. We’ll be sharing the latest news, trends, and best practices for maximizing your savings and planning for a secure financial future. Whether you’re just starting to plan for retirement or you’re a seasoned saver, this newsletter is your go-to resource for staying ahead of the curve. So, get ready to dive in and learn all about the latest in retirement planning.

Timing of Deposits 401(k)/403(b) Deferrals and Loan Repayments

New Information on Participation Statements: Lifetime Income Illustrations

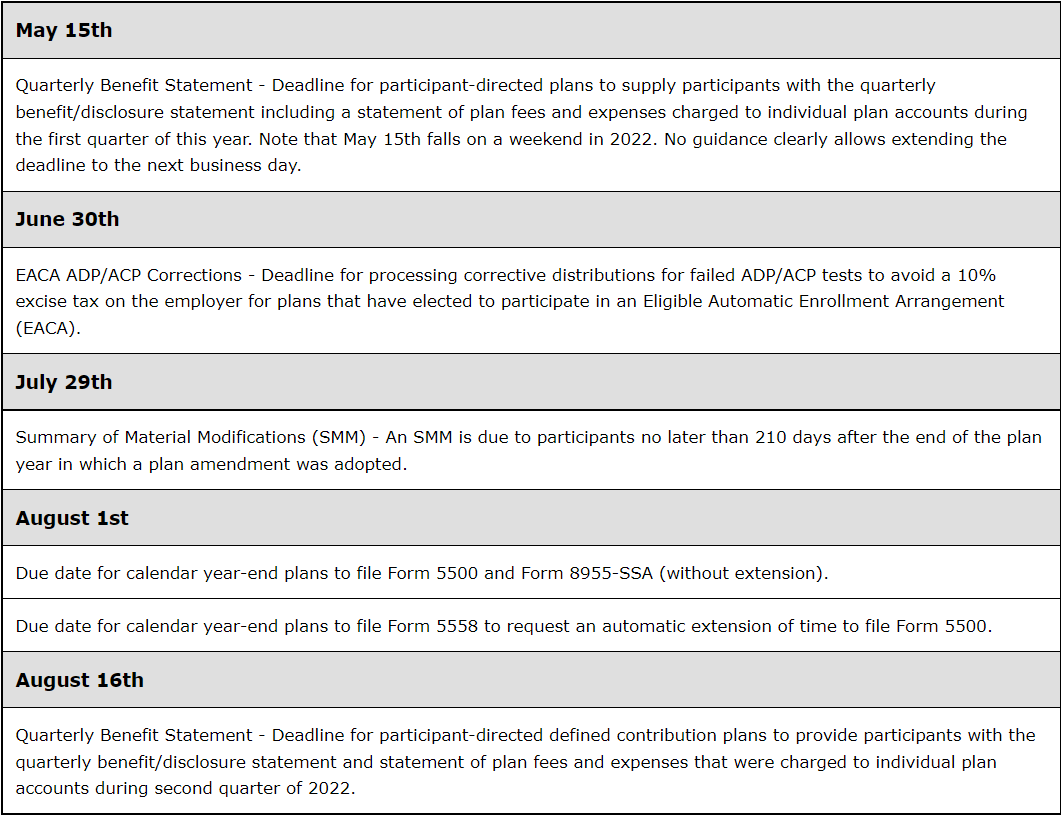

Upcoming Compliance Deadlines for Calendar -Year Plans

Timing of Deposits401(k)/403(b) Deferrals and Loan Repayments

One of the questions asked by your TPA during the annual census collection may be whether your participant contributions and loan payments were transmitted within the Department of Labor (DOL) safe harbor time frame.

It’s an important question because both the DOL and the Internal Revenue Service (IRS) are interested in seeing employee contributions deposited timely. When contributions are not deposited timely, an operational failure occurs, which could lead to plan disqualification. However, there are ways to correct the failure as well as ways to prevent future occurrences.

The following are a few scenarios that may trigger late deposits:

- Depositing a few pay dates together, later in the month, when you finally have time.

- Depositing late because you were waiting for cash flow to deposit the match at the same time.

- The employee who handles deposits is on vacation and no one else knows the process.

- Starting a deposit submission but getting sidetracked and failing to finish the submission.

The general rule is that employee contributions and loan repayments must be remitted to the plan by the earlier of:

- The date when contributions/loan repayments can reasonably be segregated from the employer’s general assets. (Most 401(k) and 403(b) plans will fall into this category.)

OR

- The 15th business day of the next month.

The number of participants in your plan also affects the permitted time frame.

- If your plan has under 100 participants as of the beginning of the plan year, no later than the 7th business day following the paycheck date is considered timely.

- If your plan has 100 or more participants, though, you likely have less time. In this case, contributions must be remitted on the earliest date possible instead of within 7 business days. If you can make the deposit on the 2nd business day after the paycheck date, for example, that is going to be the standard that the DOL feels is timely for your plan.

Having contributions remitted late to the plan could also cause additional issues for the plan. Depending on the contribution amounts involved and the fluctuation of investment returns around the time of the late deposits, this could lead to potential lawsuits by participants. Also, since the late deposit amount is reported on the Form 5500, it is a possible red flag for IRS and/or DOL audits, unless their correction programs are used. Since your TPA completes additional work to assist with the calculation and correction of late deposits, you may also incur additional administration fees.

If you discover that you missed a deposit, reach out to your TPA for assistance in determining if it is late and what options are available for correction. Your TPA will be able to explain the correction programs available and provide assistance, but ultimately it will be the plan sponsor or fiduciary who decides how to proceed. If the late deposit is discovered during an IRS audit, the Audit Closing Agreement Program (Audit CAP) option uses similar correction steps but involves negotiated sanctions.

How you choose to correct the failure will likely depend on the severity of the failure, such as the number of participants affected, the number of deposits that are late, and the contribution amounts that are late. Late deposit correction options are described below.

Self-Correction Program (SCP) – IRS Employee Plans Compliance Resolution System (EPCRS)

This option is available without contacting the IRS, but you must have procedures in place, and you must review them to determine what changes are needed to avoid the issue in the future.

- Determine which deposits were late.

- Calculate lost earnings to be deposited to affected participants’ accounts.

- Report the late deposit amount on Form 5500 for the year of the failure through the year of correction.

- In addition to the error being an operational failure, it is also considered a prohibited transaction because it is believed to be a loan from the plan to the employer. For 401(k) plans (but not 403(b) plans), this requires payment of a 15% excise tax on the calculated lost earnings using Form 5330.

Voluntary Correction Program (VCP) – IRS Employee Plans Compliance Resolution System (EPCRS)

- Complete the same action steps as SCP above.

- Submit the necessary application to describe the failure and the correction.

- The user fee varies from $1,500 to $3,500, depending on the plan’s asset balance.

- Once the submission is reviewed, the IRS issues a Compliance Statement if the correction methods were approved or if additional steps are required for correction.

DOL’s Voluntary Fiduciary Correction Program (VFCP)

- Complete similar steps as above to determine which deposits were late, and deposit lost earnings to applicable participants’ accounts.

- The completion of an application is also required, but no user fee is due.

- Some corrections may qualify for exemption from the payment of the 15% excise tax.

There are ways to avoid late deposits!

- Revisit your process. If you don’t really have one, now is the time to create one.

- Who is responsible for making the deposit?

- Who is the back-up person if the usual employee is out?

- How many days after the paycheck do you intend to make the deposit?

- Who will review the transaction confirmation to be sure it’s completed?

- Find consistency. If you have payroll on Fridays, for example, and you remit your payroll taxes on the following Tuesday, submit the contributions to the plan on Tuesday as well.

- Ask a third party for help! Your CPA, TPA, or payroll company may offer contribution remittance services. Reach out to one of them for options and pricing. Maybe the person-by-person details can be remitted to the plan’s investment platform on your behalf, and you will simply need to login to review the data and remit the payment portion.

Please note that employer contributions do not have the same timing requirement that employee contributions and loan repayments have. Employee contributions and loan repayments being withheld from your employees’ paychecks should be deposited to their accounts on time. The more checks and balances you have in your deposit process, the smoother it will be and the better chance your deposits will be timely. §

Additional resources for this topic:

DOL Federal Register issued 1/14/2010 Volume 75, Number 9: https://www.govinfo.gov/app/details/FR-2010-01-14/2010-430/summary

IRS 401(k) Plan Fix-It Guide (Mistake #8): https://www.irs.gov/retirement-plans/401k-plan-fix-it-guide

New Information on Participant Statements: Lifetime Income Illustrations

If you sponsor a defined contribution retirement plan, the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 now requires additional information be provided to your plan participants on their quarterly account statements. Along with their current account balance, two lifetime income illustrations must now be included once a year. This is intended to help your plan participants understand their current account balance in terms of what it means for them at retirement so they can be better prepared.

When is this required to start?

The Act’s interim final rule was issued on 9/18/21 and the first illustration must be provided within 12 months of that date. The start date will depend on the type of accounts included in your plan.

- Participant-directed accounts which receive quarterly benefit statements: Illustrations must be included on the 6/30/22 quarterly statement (if not already provided on the 3/31/22 statement).

- Non-participant-directed accounts: Illustrations must be included on the statement for the first plan year ending on or after 9/19/21 and must be furnished no later than the filing of the annual return for that year. For calendar year plans, this will be the 12/31/21 statement, furnished no later than 10/15/22.

What illustrations are required?

The following will be provided regardless of the participant’s actual marital status:

- A single life annuity (SLA): This will show a fixed monthly amount for the life of the participant, with no surviving benefit to a spouse after their death.

- A qualified joint and 100% survivor annuity (QJSA): This will show a fixed monthly amount for the life of the participant, and the same fixed monthly amount to the surviving spouse after the participant’s death.

What assumptions are used for the illustrations?

Age: 67 (or actual age, if older)

Interest rate: 10-year Constant Maturity Treasury rate (10-year CMT) as of the first business day of the last month of the statement period. The 10-year CMT approximates the rate used by the insurance industry to price immediate annuities.

Upcoming Compliance Deadlines for Calendar-Year Plans

Mortality table: Gender neutral mortality table in section 417(e)(3)(B) of the Internal Revenue Code. This is the table generally used to determine lump-sum cash-outs from defined benefit plans.

This is a sample illustration provided by DOL:

Facts: Participant X is age 40 and single. Her account balance on December 31, 2022 is $125,000. The 10-year CMT rate is 1.83% per annum on the first business day of December.

The benefit statement of this participant would show:

Current Account Balance: $125,000

Single Life Annuity: $645 per month for life (assuming Participant X is age 67 on December 31, 2022)

Qualified Joint and 100% Annuity: $533 per month for participant’s life and $533 for the life of spouse following participant’s death (assuming Participant X and her hypothetical spouse are age 67 on December 31, 2022). Source: https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/fact-sheets/pension-benefit-statements-lifetime-income-illustrations

What does this mean for you as plan sponsor?

Does your plan have to offer annuities? No, the normal form of distributions will still follow your current plan provisions. If your plan does offer annuities as a distribution option, you have options regarding which interest rate assumption to use. However, you will still need to assume age 67 (unless older), assume the spouse and participant are the same age, and show both the SLA and QJSA options.

Will the plan sponsor and fiduciary be liable if the payments at retirement are not as illustrated? No, as long as:

1) the illustrations are based on the DOL assumptions and

2) the illustrations on the statements use the DOL model language (or similar language). The model language will help explain how the calculations were prepared and that they are illustrative and not guaranteed.

Your participants may have questions about the illustrations, especially since the age, gender, and marital status used may differ from their actual situation. The illustrations also only consider the current account balance, not additional contributions and earnings that may be added to that balance over time. Recordkeepers and investment advisors (used by the plan for the participants or the participants’ own personal advisors) will be able to provide additional information since these illustrations may differ from what the participants have seen previously when estimating their future retirement benefits. Participants will need to consider all applicable information that pertains to their personal financial situation. This new requirement, though, is just one more piece of information that hopefully enables them to take additional steps to plan for a successful retirement. §

This newsletter is intended to provide general information on matters of interest in the area of qualified retirement plans and is distributed with the understanding that the publisher and distributor are not rendering legal, tax or other professional advice. Readers should not act or rely on any information in this newsletter without first seeking the advice of an independent tax advisor such as an attorney or CPA.

Top of Page

© 2022 Benefit Insights, LLC. All Rights Reserved.