Winter 2021 TRPC Newsletter brings with it a new edition, filled with important updates and news to keep you informed about your retirement plan. In addition to the latest trends and best practices, this issue will also provide a rundown of upcoming compliance deadlines. With the end of the year fast approaching, it’s more important than ever to stay on top of these deadlines and ensure that you’re maximizing the benefits of your retirement plan. So be sure to read this latest edition of the TRPC Newsletter for all the latest news, insights, and information about your retirement savings.

The MEP/PEP Debate: Are We Better Together?

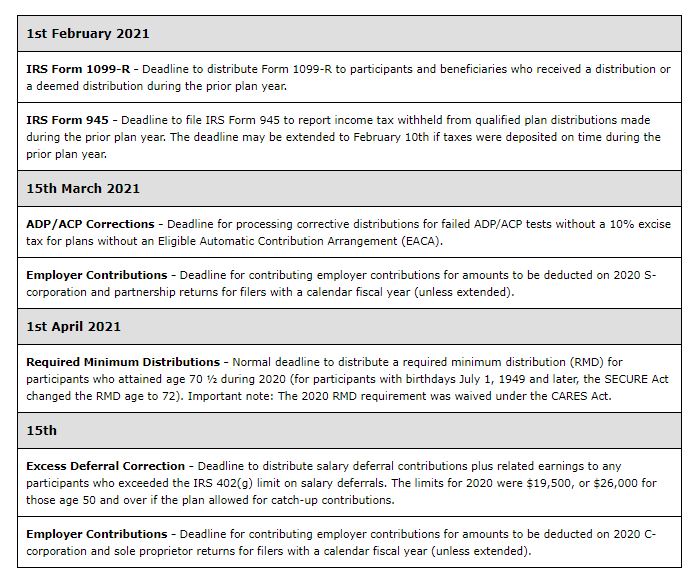

Upcoming Compliance Deadlines for Calendar-Year Plans

Terminated Employees? Important Relief is Here.

Is There Pandemic Relief For Late Deposits?

The MEP/PEP Debate: Are We Better Together?

When we talk about retirement plans, many employers think of single employer retirement plans. A single employer retirement plan is simply a plan sponsored by one employer (or a related group of employers) for the benefit of its employees. In contrast, a multiple employer plan (MEP) is a retirement plan that is sponsored by two or more unrelated employers. Historically, MEPs have allowed employers, who may not have the resources to handle a retirement plan independently, to pool together to share the administrative burden of offering a retirement plan to their employees. Although they may sound similar, MEPs are not the same as multi-employer plans. A multi-employer plan is a collectively bargained plan maintained by more than one employer, usually within the same or related industries, and a labor union.

Prior to the enactment of the Setting Every Community Up for Retirement Enhancement (SECURE) Act on December 20, 2019, all employers participating in the MEP had to share a nexus or common interest other than the retirement plan. The DOL had previously taken the position that if adopting employers did not share a common interest, the MEP was not considered to be a single plan for ERISA and Form 5500 purposes. The SECURE Act essentially reversed the DOL position by creating a new type of MEP, the Pooled Employer Plan (PEP). PEPs allow two or more unrelated employers who do not meet the regulatory commonality requirements to come together under one retirement plan.

Another welcome change provided under the SECURE Act is the elimination of the IRS’ “one bad apple” rule. In the past, the IRS took the position that if one employer ran afoul of the IRS qualification requirements, the entire MEP could be disqualified. Eliminating the one bad apple rule shields participating employers from liability from failures of the actions of a non-compliant MEP member.

While there are similarities between MEPs and PEPs, there are also many fundamental differences. A few of the key features are contrasted below.

Similarities

- Participating employers are treated as a single employer for certain purposes, such as crediting of eligibility and vesting service and plan qualification purposes.

- Participating employers are treated as separate employers for coverage, non-discrimination, and top-heavy testing purposes, and employer deduction limitations.

- In most cases, only a single Form 5500 needs to be filed. The 5500 must include an attachment that lists all participating employers along with an approximate percentage of total contributions for the year and the account balances attributable to each.

Differences

- MEPs are adopted by two or more unrelated employers that share a nexus or interest other than the retirement plan, while a PEP is adopted by unrelated employers that do not share a common interest.

- A MEP is made up of the MEP sponsor, or lead employer, and one or more participating employers, while PEPs must be operated by pooled plan providers (PPP), likely to be a financial services company, third-party administrator, insurance company, recordkeeper, or similar entity.

- The MEP sponsor generally serves as the primary administrative fiduciary for the plan, while with a PEP, the PPP is responsible for performing most administrative and fiduciary functions for the plan. In a PEP, employers retain only limited responsibility, such as selecting and monitoring the pooled plan provider, any other named fiduciaries, and investment managers. The SECURE Act requires pooled plan providers to register with both the DOL and the Treasury Department.

Proponents of MEPs are encouraged by recent changes and are hopeful that the availability of PEPs will greatly increase the number of employees covered by employer sponsored retirement plans. However, it is unclear whether they will have a significant impact on the MEP landscape. While MEPs can be attractive to employers that want to provide a retirement plan to their employees but lack the financial and administrative capacity to do so, there are potential disadvantages of which employers should be mindful. Examples of some disadvantages include the potential for increased costs due to the involvement of multiple service providers and conflicting participating employer priorities. It is important for employers to be well informed of the potential benefits and pitfalls related to participating in a MEP. It is also important to work with an experienced service provider who can provide guidance on this complex issue. ■

Upcoming Compliance Deadlines for Calendar-Year Plans

Terminated Employees? Important Relief is Here.

On December 27, 2020, the Consolidated Appropriations Act, 2021 was signed into law. The Act combines the $1.4 trillion omnibus federal spending package for the 2021 fiscal year and a $900 billion COVID-19 stimulus package that enhances and expands certain provisions of the Coronavirus Aid, Relief, and Economic Security (CARES) Act. In addition to direct stimulus payments, extending unemployment benefits to many workers, and another round of Paycheck Protection Program (PPP) loans, the COVID stimulus package includes important retirement plan relief.

Partial Plan Termination

Perhaps the most significant element of the stimulus package for plan sponsors impacted by the COVID-19 pandemic is the temporary rule preventing partial plan terminations. In general, a plan may experience a partial plan termination when turnover among plan participants exceeds 20% in a particular year, resulting in full vesting of all accounts of participants affected by the partial plan termination. Whether a partial termination has occurred is not always an easy call. The IRS makes it clear that the determination is based on the facts and circumstances of the particular scenario.

The IRS previously provided guidance to clarify that generally, employees who had been furloughed or laid off due to COVID-19 but were rehired by the end of 2020 would likely not be treated as having an employer-initiated severance for the purposes of determining a partial plan termination. However, the Consolidated Appropriations Act includes the following temporary rule regarding partial plan terminations:

“A plan shall not be treated as having a partial termination during any plan year which includes the period beginning on March 13, 2020, and ending on March 31, 2021, if the number of active participants covered by the plan on March 31, 2021 is at least 80% of the number of active participants covered by the plan on March 13, 2020.”

It is important to note that the 80% count does not have to be comprised of the same participants that were initially terminated. However, the plan’s eligibility requirements should be taken into consideration.

The new relief is based on 80% of the “active participants.” If the employees include new hires (e.g., the laid-off employees found other jobs), whether they count towards the 80% depends on the eligibility conditions of the plan. If the new hires do not satisfy the plan’s eligibility conditions by March 31, 2021, they cannot be included in the active participant count.

Active participants were not defined in the bill. Presumably, active participants include employees eligible to defer, even if they choose not to do so.

Qualified Disaster Distributions Extended

The Act includes a temporary extension for individuals to take a retirement plan distribution or loan if they reside in a presidentially declared disaster area. The extension is effective for 60 days after the date of enactment and applies to individuals residing in presidentially declared disaster areas (other than COVID-19) declared after Dec. 31, 2019. Participants in 401(k), 403(b), money purchase, and government 457(b) plans may take an aggregate distribution up to $100,000 without incurring the 10-percent additional tax on early distributions. Income tax on these distributions may be spread ratably over a three-year period, and participants may repay the distribution into a plan that accepts rollovers within three years.

Note that qualified disaster areas are areas where a qualified disaster was declared, but do not include areas that are disaster areas solely due to the COVID-19 pandemic.

Qualified Disaster Loans

The Act also enables qualified individuals to receive plan loans up to $100,000 or 100% of the participant’s vested account balance. Additionally, the repayment period is extended for up to one year (or up to 180 days after enactment of the Act, if longer) if repayment of the loan normally would be due during the period beginning on the first day of the disaster period and ending 180 days from the last day of the incident period.

Paycheck Protection Program (PPP) Round 2

The Act provides increased PPP funding and eligibility to those small businesses that have been hit hard by the COVID-19 pandemic. The Act extends the PPP through March 31, 2021 and allocates additional funds for forgivable loans. Among other important changes, the law allows eligible borrowers a second PPP forgivable loan for small businesses and non-profits with 300 or fewer employees that can demonstrate a 25% loss of gross receipts in any quarter during 2020 when compared to the same quarter in 2019. ■

Is there Pandemic Relief for Late Deposits?

Proper handling of employee 401(k) deferral contributions and loan repayments is one of the most important responsibilities a plan sponsor undertakes. Failure to timely deposit employee deferrals and participant loan repayments is considered by many service providers to be one of the most commonly made retirement plan errors. Although it may be a common error, the IRS and DOL consider timely deposits a top priority. If loan repayments and/or salary deferrals are deposited outside of the timeframe described below, the company is considered to have committed a “prohibited transaction” by being in possession of plan assets. The DOL treats this as a loan from the plan to the employer which is prohibited by law and requires a documented correction process.

What is the deadline to deposit employee deferrals and loan repayments?

Once withheld from the participant’s pay, deferrals and loan payments become plan assets as soon they can be “reasonably segregated” from the employer’s general accounts. As a result, employee deferrals must be deposited by the earlier of the date that the contributions can be reasonably segregated from the company’s general assets, or the 15th business day of the month following the month in which the pay date occurs.

For plans with fewer than 100 participants on the first day of the year, the DOL created a safe harbor standard that states that any deposits made within seven business days of a pay date are considered timely even if the deposits could have been made earlier. Unlike small plans, large plans cannot rely on the safe harbor deadline. For large plans, the DOL states that elective deferrals must be deposited “as soon as administratively feasible.” It is important to note that the DOL will often look at the actual deposit history when determining the deposit deadline and, if the company made deposits more quickly, will set that as the deadline for all other deposits. For example, if a company ever made a deposit within one or two days following a pay date, the DOL may take the position that all of the deposits should have been made within one or two days.

Was relief provided due to the COVID-19 pandemic?

On April 29, 2020, the DOL issued EBSA Disaster Relief Notice 2020-01 in response to the COVID-19 pandemic. The Notice provided guidance intended to relax the rules related to the required timeframe to deposit employee salary deferral contributions and loan repayments.

The Notice states that “the Department recognizes that some employers and service providers may not be able to forward participant payments and withholdings to employee pension benefit plans within prescribed timeframes during the period beginning on March 1, 2020 and ending on the 60th day following the announced end of the National Emergency. In such instances, the Department will not – solely on the basis of a failure attributable to the COVID-19 outbreak – take enforcement action with respect to a temporary delay in forwarding such payments or contributions to the plan. Employers and service providers must act reasonably, prudently, and in the interest of employees to comply as soon as administratively practicable under the circumstances.”

If an employer was unable to deposit elective deferral contributions timely “solely on the basis of a failure attributable to the COVID-19 outbreak,” it is important that documentation related to the late deposits (e.g., dates and amounts of each late deposit, names of affected participants, record of the specific situation(s) that resulted in the late deposits, etc.) is retained with the plan records in the event of an IRS or DOL plan audit.

What happens if deferrals were not deposited timely?

When employee deferrals are not deposited timely, there are two available correction methods. The error can be corrected under the IRS’ self-correction program, which allows plan sponsors to correct certain plan failures without contacting the IRS or paying a user fee, or by completing a filing through the DOL’s Voluntary Fiduciary Correction Program (VFCP). It is important to note that the DOL does not recognize self-correction for late deposits. However, in certain circumstances, the DOL may accept self-correction if the following steps have been completed.

- Determine which deposits were late and calculate lost investment earnings.

- Deposit any missed elective deferrals, along with lost earnings, into the trust.

- File Form 5330 with the IRS to pay an excise tax.

- Report the late deposits on the Form 5500.

- Review procedures and correct deficiencies that led to the late deposits.

What can be done to avoid late deposits in the future?

Plan sponsors can implement the following internal procedures to ensure that deferrals are deposited consistently.

- Establish a procedure requiring that elective deferrals be deposited with or after each payroll, subject to the terms of the plan document. If deferral deposits are late because of vacations or other disruptions, keep a record of why those deposits were late.

- Coordinate with your payroll provider to determine the earliest date you can reasonably make deferral deposits.

- Implement practices and procedures that you explain to new personnel to ensure that they know when deposits must be made.

As with many retirement plan compliance matters, the rules related to depositing employee deferrals and the related corrections are complex topics. If you have questions regarding the general rules or plan corrections outlined above or would like to discuss how these rules impact your plan, please contact your plan representative. ■

This newsletter is intended to provide general information on matters of interest in the area of qualified retirement plans and is distributed with the understanding that the publisher and distributor are not rendering legal, tax or other professional advice. Readers should not act or rely on any information in this newsletter without first seeking the advice of an independent tax advisor such as an attorney or CPA.

Contact us for more information.